BLOCKCHAIN: Welche Art der Verwahrung für welche Token?

Bei der Organisation der Verwahrung von Kryptowährungen oder anderen Kryptowerten (auch Token genannt) müssen bestimmte Besonderheiten berücksichtigt werden, z. B. das Fehlen eines für Kryptowerte identifizierten Emittenten oder die mangelnde Kontrolle über den Verwahrungsprozess.

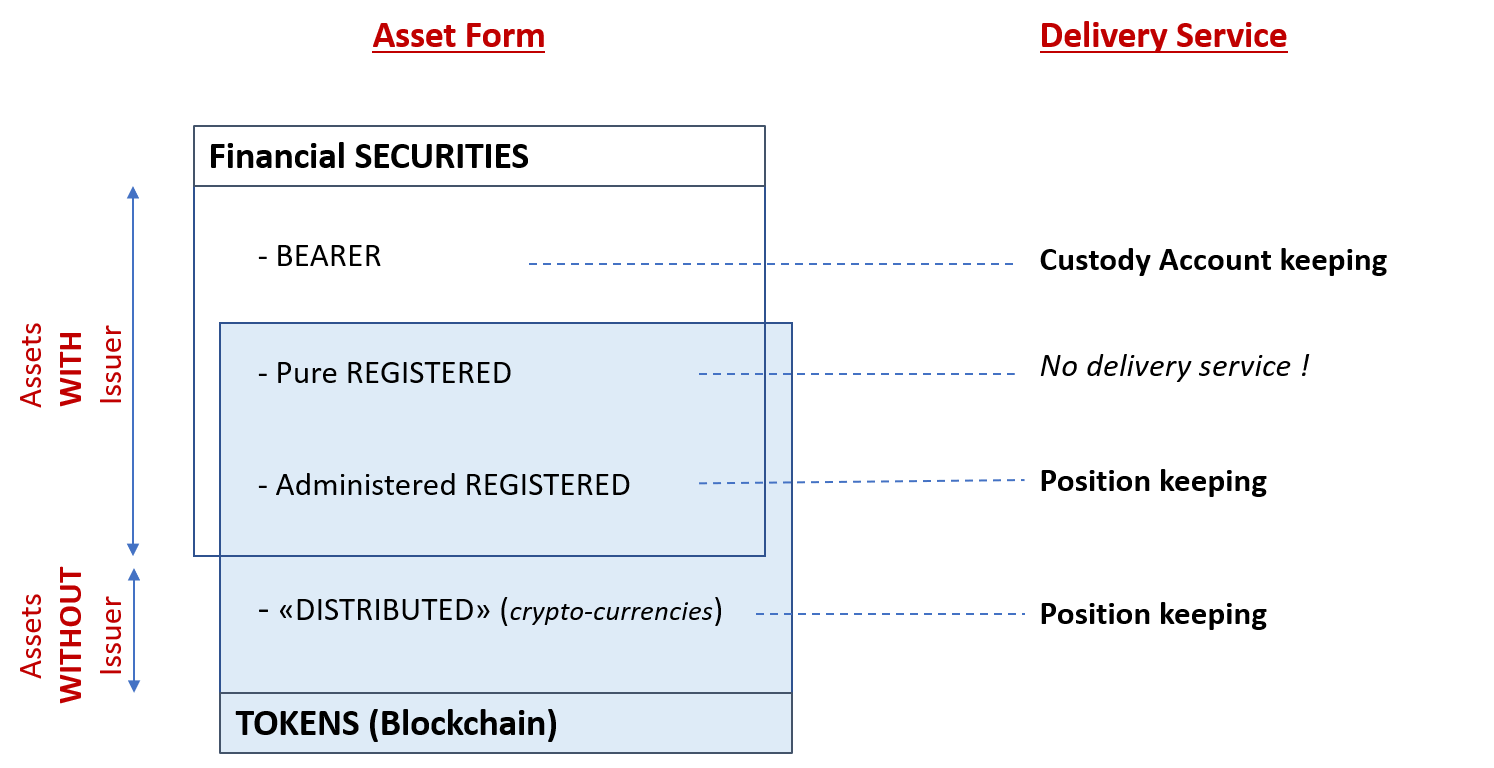

Seit der Entmaterialisierung der Wertpapiere im Jahr 1984 wird das Eigentum der Finanztitel in Frankreich durch eine Eintragung in einem Wertpapierdepot festgehalten. Gehalten wird dieses Depot:

entweder von einem autorisierten Finanzintermediär, einem sogenannten „Teneur de Compte-Conservateur“ (TCC) bzw. einer Verwahrstelle, in diesem Fall spricht man von Inhaberpapieren, da die Identität des Inhabers dem Emittenten anlässlich der Transaktionen mit diesen Titeln nicht mitgeteilt wird;

oder vom Emittenten der Wertpapiere selbst, in diesem Fall spricht man von Namenspapieren, da der Emittent die Identität des Anlegers kennt. Wenn der Anleger einen Intermediär beauftragt, sein bei einem Emittenten eröffnetes Depot zu verwahren, spricht man von „verwalteten Namenspapieren“; ohne Intermediär handelt es sich um „reine Namenspapiere“.

Namenspapiere erleichtern die Beziehungen zum Emittenten, während Inhaberpapiere die Übertragung des Eigentums vereinfachen und beschleunigen. In jedem Fall haftet die Person, die das offizielle Wertpapierdepot hält (Emittent oder Intermediär) dem Endanleger gegenüber und garantiert ihm die Möglichkeit, die Rechte im Zusammenhang mit dem Eigentum des Wertpapiers während dessen Laufzeit auszuüben. Die Tatsache, dass der Anleger die Verwahrstelle nach eigenem Ermessen wechseln kann, setzt voraus, dass die Verwahrstelle jederzeit in der Lage sein muss, die Wertpapiere ihrem Eigentümer zurückzugeben. Die Garantie der Verwahrstelle ist selbstverständlich nur möglich, wenn die Verwahrstelle die technischen Instrumente beherrscht, die diese Verwahrung sicherstellen.

Der Fall von Kryptowährungen

Da diese Kryptowährungen keinen Emittenten haben, ist die Verantwortung für die Führung des Emissionsregisters nicht mehr auf eine einzige Einheit beschränkt, sondern auf die Gemeinschaft der Kryptowährungsinhaber "verteilt".

Das sogenannte Loi PACTE, das am 11. April 2019 in Frankreich verabschiedet wurde, hat dieses Postulat mehr oder minder in Frage gestellt, indem es einen Verwahrdienst der digitalen Vermögenswerte (andere Bezeichnung für Token) zu definieren versucht, wobei der Dienstleister generell nicht in der Lage ist, das System zu verwalten, das die Übertragung des Eigentums an den Vermögenswerten sicherstellt. Das System beruht auf der Blockchain-Technologie, die ursprünglich eigens für die Übertragung und die Verwahrung der berühmten Kryptowährungen wie Bitcoin oder Ether entwickelt wurde. Da diese Kryptowährungen nicht wirklich einen Emittenten haben, wird das Register nicht mehr zentral von einem Unternehmen geführt, sondern auf eine Gemeinschaft von Kryptowährungsinhabern „verteilt“ (Bestätigung der Transaktionen durch Konsens der Inhaber). Aus diesem Grund ist diese Verteilung der Verantwortung für die Verwahrung der Vermögenswerte schließlich eher eine Ergänzung als eine Alternative zu Inhaber- und Namenspapieren, da sie für Wertpapiere ohne Emittenten gilt, die nicht von den alten Systemen berücksichtigt werden.

Von der Depotführung bis zur Positionsführung

Einem Dienstleister ist es also nicht möglich, ein klassisches Depot im Namen Dritter für Kryptowährungen zu führen, weil er das Verwahrsystem der Kryptowährungen nicht beherrscht. Er kann jedoch weiterhin eine Position führen, das heißt prüfen, dass die Menge Kryptowährungen, die auf der Ebene der Blockchain anerkannt wird, tatsächlich den Transaktionen, von denen er Kenntnis hat, entspricht. Die Positionsführung ist kein neues Konzept, denn sie wird bereits im Rahmen der Verwahrung verwalteter Namenspapiere angeboten. Es besteht jedoch ein deutlicher Unterschied zwischen einer Positionsführung für Kryptowährungen und einer Positionsführung für klassische Wertpapiere (d.h. mit einem Emittenten). Bei klassischen Wertpapieren kann sich der Positionsführer an den Emittenten wenden, wenn die Position ihm nicht richtig vorkommt und er den Unterschied nicht verantwortet. Für Namenspapiere besitzt der Emittent die Fähigkeit, alle Anomalien in seinen eigenen Verzeichnissen selbst zu regeln. Ohne Emittent ist dieser Rückgriff bei Kryptowährungen leider nicht möglich.

Die Positionsführung für Dritte in einer Blockchain setzt selbstverständlich voraus, dass man die Zugangsmittel zu den Token des Dritten in dieser Blockchain besitzt, beispielsweise die kryptografischen Schlüssel.

Der Fall von Hilfs- oder Sicherheitstoken

Manche Blockchains wollen jedoch auch andere Vermögenswerte verwalten als ihre ursprünglichen Kryptowährungen. Das ist der Fall der Utility Token oder der Security Token, die trotz der unterschiedlichen Rechte (Nutzungsrechte vs. Finanzrechte) etwas gemeinsam haben, nämlich einen Emittenten.

Die Gegenwart dieser Emittenten in der Blockchain erfordert, dass ihnen gegenüber der Gemeinschaft der einfachen Anleger bestimmte Rechte auf ihre eigenen Verzeichnisse gewährt werden. Die ausschließliche Verteilung der Verantwortung auf die Anleger hat also keinen Sinn mehr. Man muss die Blockchain und Namensverwahrung gemäß Artikel R211-2 Code Monétaire et Financier kombinieren. Diese Kombination der verteilten Verzeichnisse und der Namensverwahrung erfolgt nicht sofort und dürfte IT-Entwicklungen (Smart Contracts?) und/oder entsprechende Zulassungen voraussetzen, je nachdem, ob man es mit einer öffentlichen Blockchain (allen zugänglich mit nur einem Teilnehmerprofil) oder einer privaten Blockchain (einigen Teilnehmern mit möglicher Differenzierung der Profile vorbehalten) zu tun hat.

Internationale Standards

Fazit: Es wäre besser, bei Token von Positionsführung statt von Verwahrung zu sprechen, auch wenn, wie wir gesehen haben, die Positionsführung der Token auf der Verwahrung der Zugangsmittel zu diesen Token beruht. Da das Thema nicht nur Frankreich und die französische Gesetzgebung betrifft, wäre es wohl wünschenswert, dass die nötigen Anpassungen für die Berücksichtigung der Emittenten der Blockchains Gegenstand von Standards auf mindestens europäischer, wenn nicht sogar internationaler Ebene sind.